HARNESSING THE POWER OF ADVANCED ANALYTICS

HARNESSING THE POWER OF ADVANCED ANALYTICS

HARNESSING THE POWER OF ADVANCED ANALYTICS

HARNESSING THE POWER OF ADVANCED ANALYTICS: UNLOCKING CUSTOMER NEEDS AND PREFERENCES FOR INSURANCE COMPANIES

The funding in the Insurtech sector increased from $4.9 billion USD in 2018 to a whopping

$16.7 billion USD in 2021 worldwide. The stagnant insurance industry is now changing;

increased customer demands, disruptive technology, fast adaption rates, the advent of

artificial intelligence, the significance of customer experience, availability of data, machine

learning, and optimized data analytics techniques have collectively transformed the

insurance business environment.

This era of disruptive technological advancement has increased customer power

significantly. Customer satisfaction is the goal of any service provider. The insurance industry

has also realized the immense potential of customer power and is working relentlessly to

improve user journeys. The insurance industry is driving from reactive techniques to

preventive measures. The sophisticated advanced analytics (AA) tools and techniques help

minimize fraudulent activities, personalize plans and charge premiums, and provide realistic

underwriting through machine learning. AA is a complete package tool that helps measure,

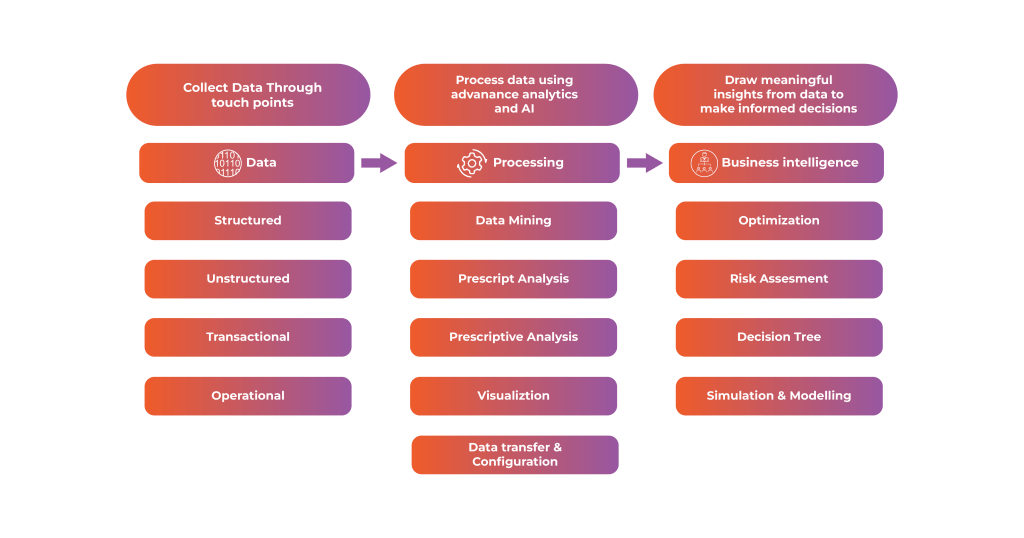

predict, and optimize organizational performance. Ranjit Bose, the Regents’

Professor of Management Information Systems at the Anderson School of Management of

the University of New Mexico, has put forward a three-fold foundational infrastructure

proposal for implementing AA (Artificial Intelligence and Analytics) within any organization.

Foundational Infrastructure Proposal for AA Implementation in Insurance Industry

These AA tools should be integrated across the functional units of the insurance organization to

deliver results. Insurance companies have access to various data points. However, the true

value lies in using these data points to make effective decisions. Turning data into useful key

insights is only possible by AA. Researchers have identified the following use cases of the

implementation of big data in the insurance sector that improves customer satisfaction.

USE CASES OF ADVANCED ANALYTICS TO ENHANCE CUSTOMER SATISFACTION

CUSTOMER SEGMENTATION AND PERSONALIZATION

Customers of today have ephemeral brand loyalties. They are constantly on the lookout for new

experiences and better products. Digitization has facilitated effortless accessibility and reduced

switching costs for the customer. Previously, customers primarily compared insurance plans

based solely on price, opting for the lowest option. However, the current trend indicates that

customers now prioritize enhanced consumer journeys and better experiences. As a result,

insurance companies have been compelled to transition from a product-centric mindset to a

customer-centric approach. The art of understanding the needs of various customer segments

and predicting their buying behavior lies in effective segmentation.

Advanced analytics unlocks limitless segmentation potential by handling 1000s of data sets

simultaneously. Traditionally, limited data sets, time consumption, human constraints, and

biases restrict segmentation. Machine learning algorithms and advanced visualization

techniques process real-time data instantly and provide a picturesque representation of data

which makes decision-making effective and efficient.

Segmentation identifies the right product for the right customer segment. Clustering techniques

are widely used to classify customers. Some segmentation frameworks are coined below to

understand the role of AA for customer satisfaction.

CUSTOMER SEGMENTATION FRAMEWORK USING RECENCY, FREQUENCY, AND MONETARY (RFM) AND CUSTOMER'S LIFETIME VALUE (LTV) MODELS FOR BANKING MARKETING STRATEGIES

A structured framework has recently been developed to apply Recency, Frequency, and

Monetary (RFM) customer’s lifetime value (LTV) models. This framework utilizes customers’

demographic data to segment banking customers and create effective marketing strategies. The

analysis study comprises two main phases: in the first phase, CRM data is employed to cluster

the customers, and in the second phase, demographic data variables such as age, education,

and occupation, selected through the SOM technique, are used to re-cluster the segments

obtained from the first step. Both of these steps employ the K-Means clustering technique. To

optimize the customer’s value, which is one of the study’s objectives, the comparison of

customer value uses LTV instead of inter/intra cluster distances

Another researcher developed a comprehensive framework to segment customers, compute

LTV for each segment, and project their future value. Employing K-means and two-step

clustering algorithms, two levels of clustering were applied to a substantial dataset of customer

transactions, encompassing deposit type, transaction date, balance before transaction, and

transaction amount. The customer’s lifetime value was determined using the RFM model,

renowned for its simplicity and effectiveness as a customer LTV approximation model.

Additionally, the study utilized a time series method, the multiplicative seasonal ARIMA

regression, to forecast future values for each segment

Another researcher developed a comprehensive framework to segment customers, compute

LTV for each segment, and project their future value. Employing K-means and two-step

clustering algorithms, two levels of clustering were applied to a substantial dataset of customer

transactions, encompassing deposit type, transaction date, balance before transaction, and

transaction amount. The customer’s lifetime value was determined using the RFM model,

renowned for its simplicity and effectiveness as a customer LTV approximation model.

Additionally, the study utilized a time series method, the multiplicative seasonal ARIMA

regression, to forecast future values for each segment

CUSTOMER ATTRITION AND RETENTION

A lost customer is an opportunity lost. Customer acquisition costs (CACs) are much greater

than customer retention costs. It is essential to look for factors that make customers lose trust in

the brand. Advanced analytics predict trends and map pain points in customers’ journeys to

determine reasons for leaving. It is estimated that 43.6% of customers leave due to poor

service quality. An AI service bot can handle claims and assist immediately. Predictive analysis

determines the customers’ lifetime value (CLV). This determines the profitability period of a

customer. It also gives insights on when to promote or demote a certain offer. Lemonade

Insurance uses AI technology to provide personalized plans to their customers and hence a

lower churn rate than industry giants. Proceedings of the 2011 International Conference on

Industrial Engineering and Operations Management held in Malaysia highlight an interesting

use case of customer retention using advanced analytics.

UTILIZING CUSTOMER BEHAVIOR ANALYSIS FOR BANK CUSTOMER SEGMENTATION AND RETENTION STRATEGIES

A comprehensive analysis study was conducted to segment bank customers based on their

behaviors, aiding the bank in devising retention strategies and attracting new customers. The

dataset used for analysis integrates three tables: customers’ demographic data, transaction

records, and bank card data. The study considers essential information and combines attributes

such as transaction type, transaction frequency, service type, bank type, and channel type

(ATM, Web, and Terminal) with other customer attributes. The author employed Artificial Neural

Networks (ANN) to classify the factors based on their profitability.

T. L. Oshini Goonetilleke identifies the use of decision trees and neural networks to reduce

churn rate in his works titled as Mining Life Insurance Data for Customer Attrition Analysis

ANALYZING CUSTOMER DATA IN LIFE INSURANCE COMPANY CRM TO PREVENT CHURN

This research focused on life insurance company CRM data aimed to analyze customer data

and mitigate churn and attrition. The data is extracted from an operational database: the dataset

covers life insurance policies with an average term of 18-20 years, necessitating the mining of a

significant amount of historical data to build an efficient model. The study incorporated

demographic data (gender, age, profession, etc.) as well as policy details like term, sum

assured, premium, and agent information. Visualizations, Correlation-based Feature Selection

(CFS), and Information Gain techniques were utilized to select relevant attributes or attribute

combinations. The classifiers employed included the J48 decision tree and Artificial neural

network model with a standard Multilayer Perceptron. Additionally, the study addressed

challenges related to the dataset’s numerous attributes and the need for human intervention in

various stages of analysis

CUSTOMER ONBOARDING AND ENGAGEMENT

In today’s digital age, customers expect simple language, easy procedures, hands-on

applications, and immediate processing. No one wants to wait for days for a query to be

answered or a lengthy mail document filled with industry jargon to sign for a policy change to

implement. Insurance companies need to invest in easygoing yet state-of-the-art applications

and faster processing. Digital Onboarding is the need for today. It is easy on the pocket and

heavy on the heart. To drive engagement, insurance companies use channels such as video

marketing, email marketing, and interactive marketing. For example, a personalized email

message on a birthday can result in a lifetime customer a insurance policy.

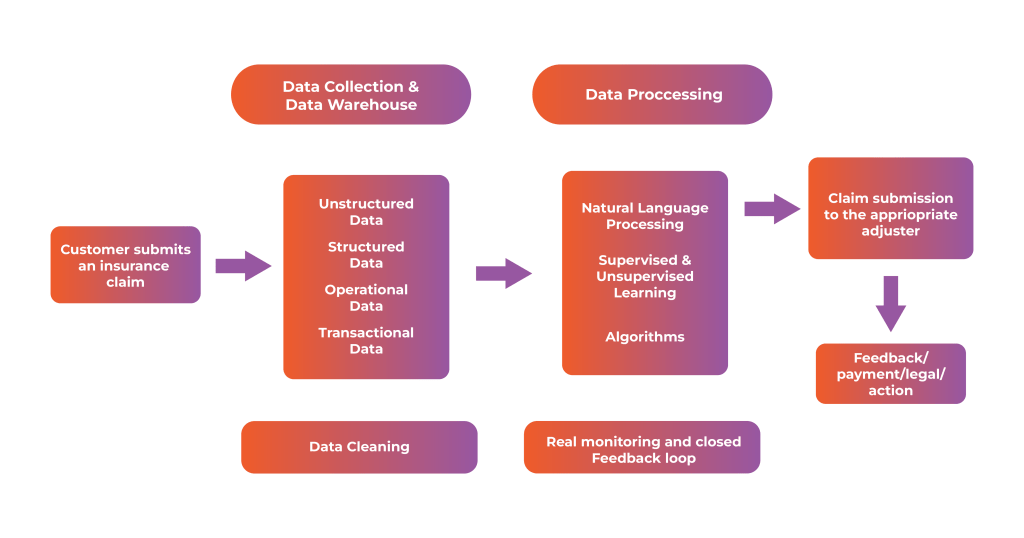

CLAIMS MANAGEMENT

Claims Management is an integral part of insurance processes. An insurance company is

responsible for managing thousands of claims every day. This is a hefty job that requires

in-depth analysis and expertise. IoT and Data management capabilities have made this easy.

Claims management software can process these claims and characterize them based on

urgency, revenue, fraud, expertise, and legal assistance required. Advanced analytics and AI

collectively can handle day-to-day claims efficiently. This saves money, resources, and time.

Claims subrogation management can be optimized using the power of analytics. Complex

mathematical models predict recovery trends, claims processing costs, and recovery potential

based on historical patterns of liability trends, litigation data, and mitigation efforts.

Simultaneously predictive and prescriptive analysis process claims information and assigns the

best-suited adjuster for the job. This reduces inefficiencies in the system and increases

customer satisfaction.

Framework for claims management using Advance Analytics

TELEMATICS AND USAGE BASED INSURANCE

Usage-based insurance has transformed the insurance industry’s outlook. Telematics is widely

used in auto insurance where a black box is installed in the car which monitors driving habits.

Additionally, data is gathered through police records, previous claims, vehicle maintenance, and

challans issued. This helps insurance companies in determining the high-value vs high-risk

customers. It also favors customers as they pay for what they are worth.

Soon telematics will begin to penetrate the home and life insurance. A customer that agrees to

potential data tracking of health records via applications or smart trackers can save an amount

on insurance. Similarly, a well-maintained house that has water sprinklers, an automated water

shut-off device, and house security control installed will have a lower insurance fee and lower

risk than a worn-out house.

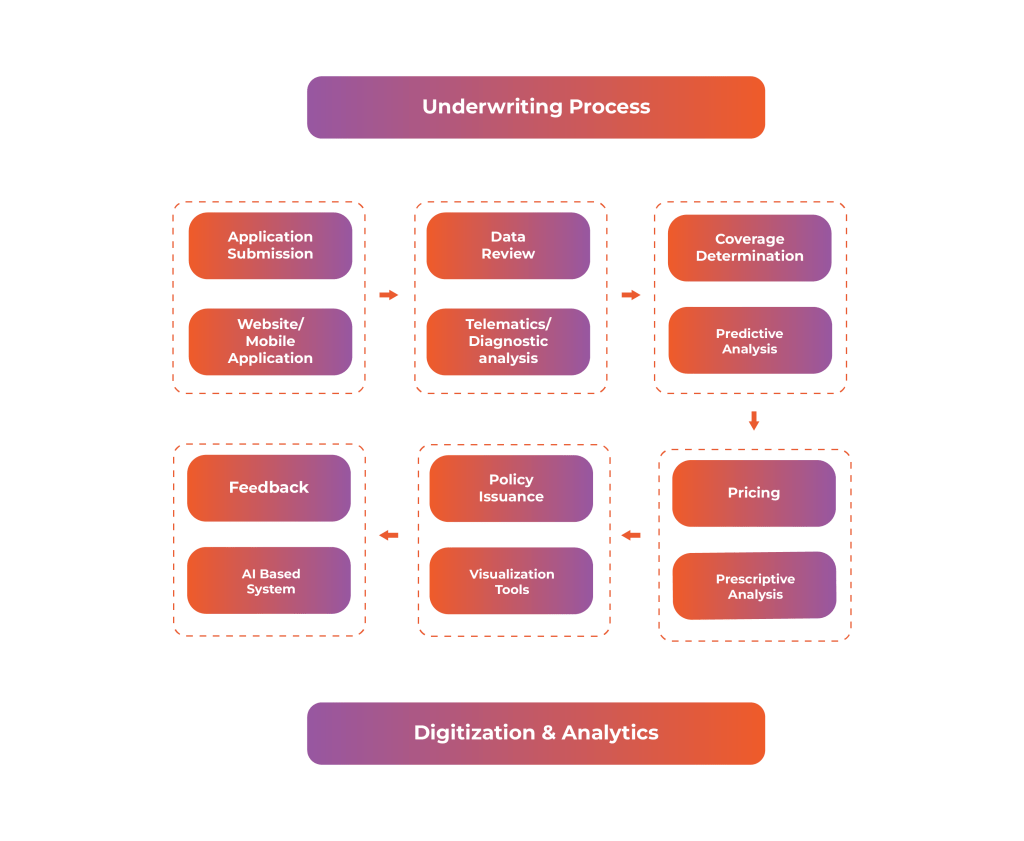

RISK ASSESSMENT AND UNDERWRITING

Risk assessment is a lucrative task, if done wrong, it would cost millions. However, a human

has limitations and can only process limited data. Advanced analytics and machine learning

have made it easy to quantify and qualify hundreds of data points at once. Multiple risk

parameters can be processed with claims data, to identify potential risk types and impacts. The

predictive models help in identifying optimized risk scoring and expense ratio to write the

correct underwriting policy. Analytics speeds up the entire underwriting process. Analytics

influence all steps of underwriting. From initial data review to final policy issuance, the use of

AA optimizes the process.

The insurance industry is growing at a CAGR of 12% and is expected to reach a market value

of $9.8 trillion (about $30,000 per person in the US) by 2027 globally. The insurance market is

submerged with new startups, out of which 53% are from the United States alone. This

exponential growth in the insurance industry makes it challenging for companies to keep their

competitive edge. Multiple options in the market and low switching costs have made customer

retention and acquisition difficult. It is important to penetrate user minds and map their journeys

to provide a better experience. The penetration of IoT & cloud computing technology has

rewired consumers to look out for a one-stop solution. Nowadays customers don’t want a car

insurance plan or a health insurance plan but a package deal. A car insurance plan that

includes car maintenance and rewards for safe driving is much more appealing than a

traditional car insurance plan. The insurance core products are losing their touch and

non-insurance products such as financial planning or home maintenance plans are in demand.

The future of the insurance industry is by preventive measures rather than reactive rewards.

Customers require instant access to information and assistance digitally via mobile applications

or websites. The use of an AI virtual bot to handle customer queries and claims will increase

customer satisfaction and reduce costs

The future of the insurance industry belongs to the insurance companies that proactively

integrate these technological advancements into their integrated systems, establish relevant

partnerships, invest in employee skills, and implement effective change management across the

entire company to leverage the full potential of these technologies. A leading insurance industry

OP Financial installed a virtual chatbot that converses in the native language to its customers

and reduces customer waiting time to zero. Together with Indian Farmers Fertiliser Cooperative

Limited (IFFCO) and the Tokio Marine Group, IFFCO Tokio General Insurance Company Limited

innovated claims handling by integrating an AI-based Claim Damage Assessment Tool that uses

computer images and neural networks to identify vehicle damages.This reduces claim

management costs by 30% and optimizes time from four hours to just fifteen minutes.

Corebridge Financials have recently partnered with Blackstone and Blackrock (Innovative

investment management solutions companies) to strengthen their business model.

These collaborations form the foundation of their innovative investment model, combining their

expertise in asset allocation determination, asset and liability management profiling, and risk

management with the expertise of world-class asset managers. Furthermore, by integrating

BlackRock’s Aladdin platform, they are revolutionizing their investment platform with expanded

analytics and accounting capabilities.The climate in the insurance industry is transforming as

more companies look for innovative solutions. In this era of disruption, innovation leads to

profitability. Big Data is a game changer for the Insurance industry. The future belongs to early

adopters and innovators. It’s either innovate today or regret later.